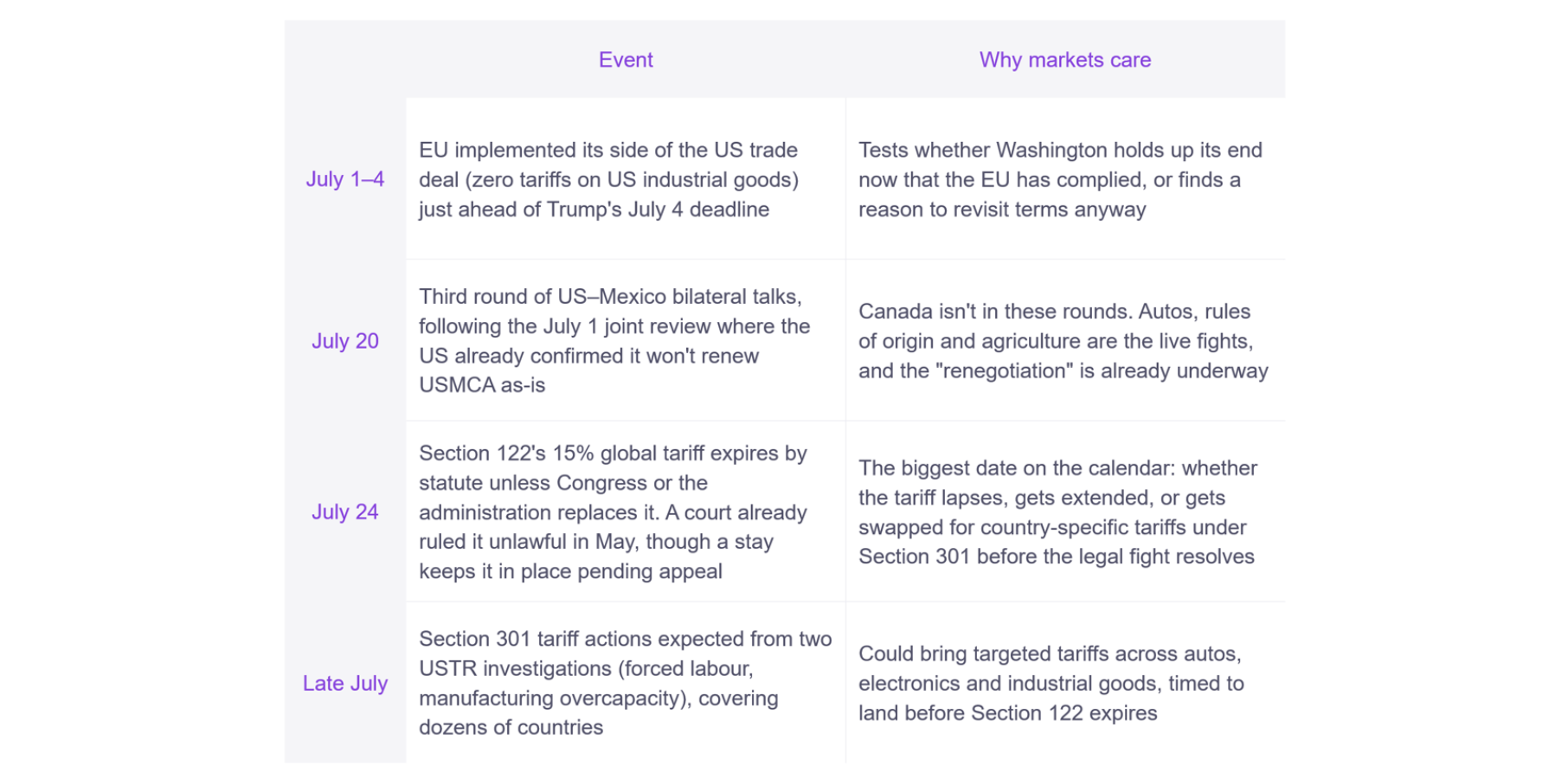

Tariff risk is back on the radar in July, with three stress points coming into play.

Three things are happening at once. First, emergency tariffs are hardening into something closer to permanent policy. Second, USMCA’s 16-year framework is starting to look more like an annual renegotiation. Third, the July 24 deadline for the Section 122 15% global tariff surcharge will test whether the measure expires, is extended, or is replaced through another tariff mechanism.

Three main observations.

Three main observations.

1. Tariffs stop being an emergency measure and become the default. Section 122 was only a stopgap after the courts struck down the original tariffs, but Section 301 may slide in to replace it before the July 24 deadline

2. Trade agreements stop being fixed and become provisional. USMCA’s July 1 review already produced a US refusal to renew as-is, a sixteen-year pact is now something renegotiated on a rolling basis

3. The TACO trade gets its first real test.

The Section 122 surcharge has run its 150-day statutory clock, expiring July 24.

For a company deciding where to build a plant or lock in a supplier, the planning horizon just got cut from “length of the treaty” to “length of the next review cycle.” Even without an adverse renegotiation of USMCA, the possibility that terms could be revisited every July is enough to make a CFO think twice before committing capital to a cross-border supply chain.

Companies used to model tariff risk once per treaty. Now they may need to model it once a year.

From a sector-specific angle, there are three points of exposure. Autos carry the most direct exposure. A vehicle can meet USMCA’s content rules and qualify for zero tariffs and still get hit by a 301 tariff if a component inside it comes from a targeted country. Industrials are the direct subject of the overcapacity investigation, so any tariffs to come out of it will be built around industrials specifically, not incidental to a tariff aimed elsewhere. Logistics sits downstream of both and tends to show trade diversion in the data before it shows up anywhere else, freight and routing numbers would give the earliest read.

July 24 also tests the TACO trade that caused much ruckus last summer. The term was coined while Trump still had the option to walk it back with an announcement, however a statutory expiry can’t be talked down the same way.

A treaty was supposed to be the stable thing and a tariff the temporary one. If both end up negotiable, the real question for August isn’t which deadline moved, but rather which assumption to stop making next.

Interested in how tariff risk could flow through to market positioning and supply chains?

Let’s Talk