Gone are the days when you could simply buy Nvidia and call it an AI strategy. The AI trade has expanded far beyond a handful of household names. What began as a story about GPUs has evolved into a broader ecosystem of suppliers, bottlenecks and infrastructure providers, many of which remain less familiar to investors. At Marex Financial Products, we’ve been exploring this landscape with clients and have broken the universe into a series of sub-themes. Think of them as galaxies.

Compute and Memory

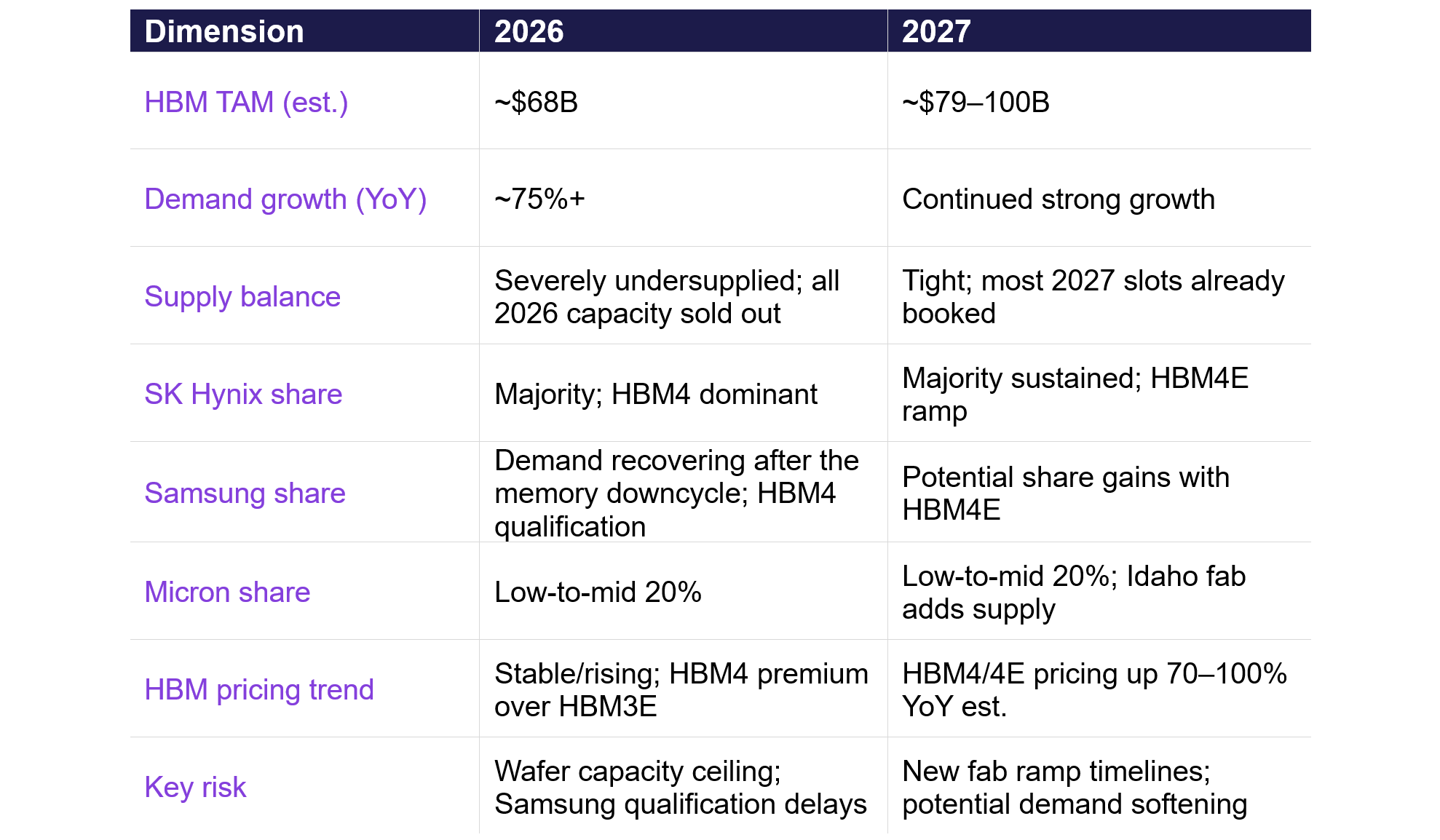

The compute buildout is accelerating, but the memory question is where it gets interesting. High-bandwidth memory (the specific type of memory that makes AI training possible at scale) has three producers globally: SK Hynix, Samsung and Micron. SK Hynix has forecast the market growing at 30% annually through to 2030, and with GPU cloud infrastructure scaling fast to meet demand that shows no sign of slowing, the memory-to-compute ratio keeps climbing. Multiyear supply visibility is increasingly locked in before products even ship.

The table below summarises why HBM has become such an important bottleneck within the AI supply chain. Demand is growing rapidly, supply remains concentrated across only a few producers, and much of the available capacity for the next two years appears to have already been committed.

Note: HBM, or high-bandwidth memory, is the specialised memory used alongside AI accelerators to move large amounts of data quickly. HBM3E is the current enhanced generation used in advanced AI systems; HBM4 is the next-generation standard for higher bandwidth and capacity; and HBM4E is expected to be the enhanced version of HBM4 for future AI platforms. A fab, short for semiconductor fabrication plant, is the highly specialised facility where silicon wafers are processed into chips.

Note: HBM, or high-bandwidth memory, is the specialised memory used alongside AI accelerators to move large amounts of data quickly. HBM3E is the current enhanced generation used in advanced AI systems; HBM4 is the next-generation standard for higher bandwidth and capacity; and HBM4E is expected to be the enhanced version of HBM4 for future AI platforms. A fab, short for semiconductor fabrication plant, is the highly specialised facility where silicon wafers are processed into chips.

Data Movement

Every chip in a cluster needs to talk to every other chip, and the speed at which that happens has become as important as the compute itself. The optical layer (transceivers, fibre, interconnects) is what makes that possible, and the market is moving fast. Over 80% of data centre links within hyperscale environments now run on optical rather than copper. The datacom optical component market grew over 60% in 2025, with 800G transceiver shipments doubling year on year, and the transition to 1.6T is already underway.

Silicon Supply

Every leading-edge AI chip starts with a silicon wafer processed through lithography equipment of extraordinary complexity. ASML holds 100% of the EUV lithography market (the machines required to manufacture chips at advanced nodes), a position built over 30 years and more than €10 billion in R&D, with no credible commercial rival. That concentration doesn’t stop at lithography. Advanced packaging, which stacks multiple chips together to behave as one, sits in similarly few hands, and the speciality materials and chemicals underpinning it all add further layers of structural tightness throughout the chain.

Power and Sites

AI-focused data centres grew electricity consumption by 50% in 2025. The IEA projects total data centre power demand to double to 945TWh by 2030, growing at 15% per year. That is four times faster than every other section combined. The industry’s response has been striking: the pipeline of nuclear offtake agreements between hyperscaler and small modular reactor projects grew from 25 gigawatts to 45 gigawatts in under a year.

None of these themes exist in isolation. The chip needs the memory, the memory needs the packaging, the packaging needs the equipment, the whole stack needs the power. The big-ticket names are not going anywhere, but the infrastructure sustaining them is where the next several years of this trade will be won.

Interested in exploring the AI sub-theme universe?

Let’s Talk

Lexicon

GPU: A graphics processing unit. Originally used for graphics, now central to AI because it can process many calculations in parallel.

HBM: High-bandwidth memory. A specialised form of memory used alongside AI chips to move large amounts of data quickly.

DRAM: Dynamic random-access memory. A common type of computer memory used across servers, PCs and data centres.

Wafer: A thin slice of silicon used as the starting material for manufacturing semiconductors.

EUV Lithography: Extreme ultraviolet lithography. The highly specialised chipmaking technology needed to produce the most advanced semiconductors.

Advanced Packaging: The process of combining multiple chips or memory components into one high-performance package.

Optical Transceivers: Components that convert electrical signals into optical signals, helping chips and servers move data at high speed.

Hyperscalers: Large cloud and technology companies operating massive data centres, such as Microsoft, Amazon, Google and Meta.

SMR: Small modular reactor. A next-generation nuclear reactor designed to be smaller and more flexible than traditional nuclear plants.

Baseload Power: Reliable power that can run continuously, making it important for energy-intensive infrastructure such as data centres.